Where Marty Weitzman Went Wrong

There are no solutions. There are only trade-offs.[Thomas Sowell]

WARNING: This post is full of technical gobbledygook.

The Gordian Knot News has multiple audiences. The main one is my favorite person: the open minded, inquiring soul who has not been over-indoctrinated by our “educational” apparat. For these people, we assume a decent grasp of high school algebra and nothing else. Nothing else is needed for the GKN’s core argument: we must have near should-cost nuclear to solve the Gordian Knot.

A secondary audience is people who have specialized training in engineering, or economics, or biology. Occasionally to refute this or that claim, the GKN must reluctantly get technical and descend into the jargon of this or that specialty to make the argument. This is one those posts.

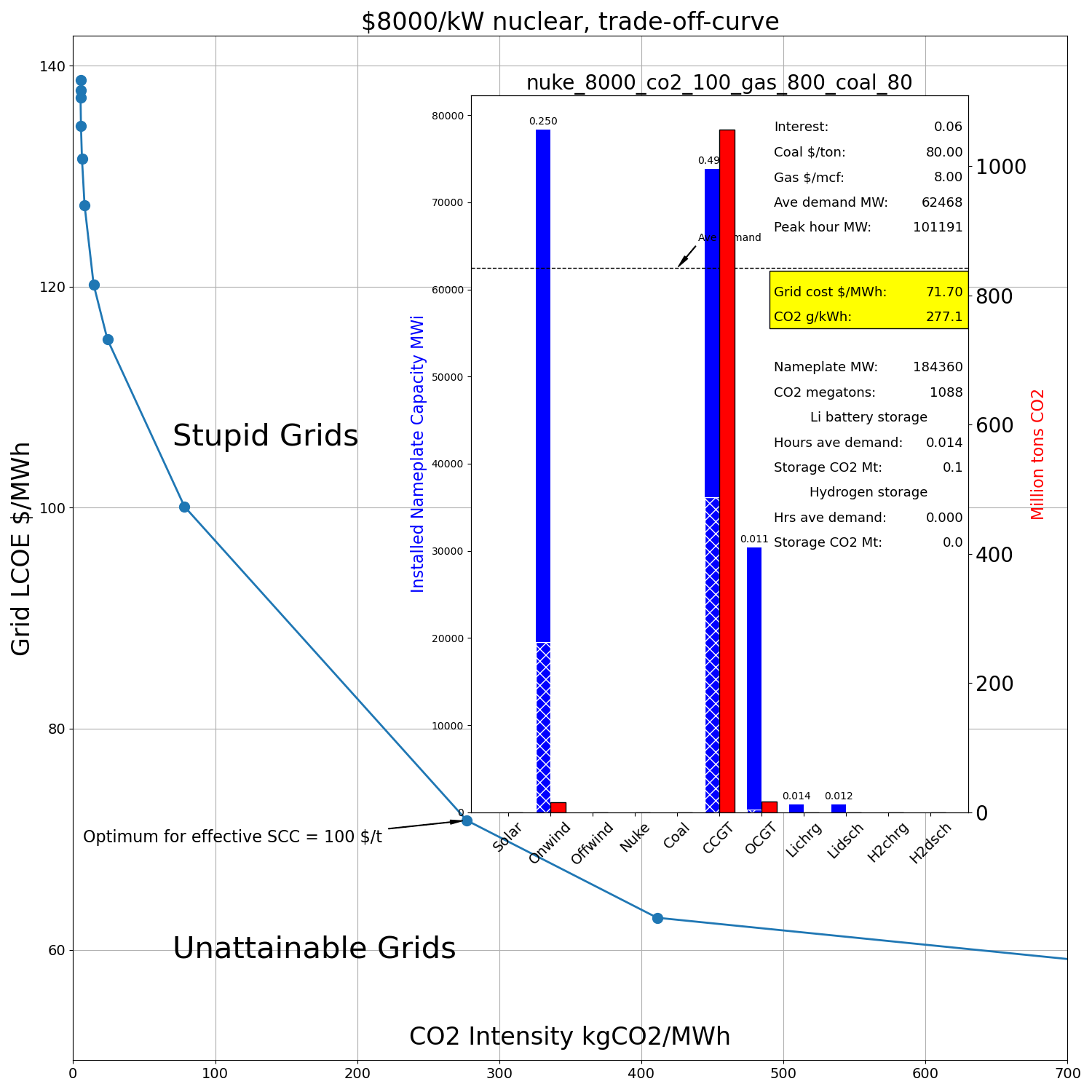

Figure 1. Germany’s power grid trade-off curve if the overnight cost of nuclear is $8000/kW. The region to the northeast of the curve contains stupid grids. The region to the southwest is technologically unattainable. The inset shows the optimum grid for this nuke cost and a Social Cost of CO2 of $100/ton. Each point on the trade-off curve will have its own optimal grid.

Marty Weitzman was one of the most influential economists of the very late 20th century. He died in 2019 at the age of 77. Although our times at MIT overlapped, I cannot recall ever meeting Weitzman. But I have talked to people who knew him. They all agree that not only was he exceptionally brilliant; but he was also a super nice human being. Some of his most important work was on how to handle the uncertainties we have about global warming.

This is a critically important subject on which the Gordian Knot News has ruminated in at least 5 posts. If you are interested, you should read them in this order:

1) Should Cost nuclear and human ignorance.

2) The Mother of all Tragedies.

3) Expensive nuclear power’s dirty secret.

4)Thinking quantitatively about CO2 uncertainty.

5) A modest proposal for resolving our differences on CO2.

Weitzman argued strongly for using fat-tailed probability densities to represent our uncertainty about the impact of global warming. Thin-tailed densities, such as the Normal, decrease exponentially or faster, as you move to less and less likely outcomes. The decrease is fast enough, so that, if you are far enough away from the most probable outcome, the probabilities are so low that for practical purpose they can be ignored.

Weitzman argued that, given the existential implications of a planet temperature increase of say 20C, such outcomes could not possibly be negligible. He claimed we must use fat-tailed densities, densities that decrease like a power law in the high end tail. The Gordian Knot Group agrees. We usually use a log-normal density to model our uncertainty about global warming. The log-normal is fat-tailed.

But Weitzman then went too far. He claimed that such densities made conventional cost-benefit analysis close to meaningless.

Perhaps in the end the climate-change economist can help most by not presenting a cost-benefit estimate for what is inherently a fat-tailed situation with potentially unlimited downside exposure as if it is accurate and objective --- and perhaps not even presenting the analysis as if it is an approximation to something that is accurate and objective –-- but instead by stressing somewhat more openly the fact that such an estimate might conceivably be arbitrarily inaccurate depending upon what is subjectively assumed about the high-temperature damages function along with assumptions about the fatness of the tails and/or where they have been cut off.\cite{weitzman-2009}[p 26]

This is a polite way of saying the results are useless. I’ll call this Weitzman’s Useless Proposition. Weitzman pointed out that the ratio of a fat-tailed density to a thin-tailed goes to infinity at the high end; but he never proved the Useless Proposition. Nor, despite his mathematical prowess, could he. It is in fact false for a wide range of fat-tailed densities.

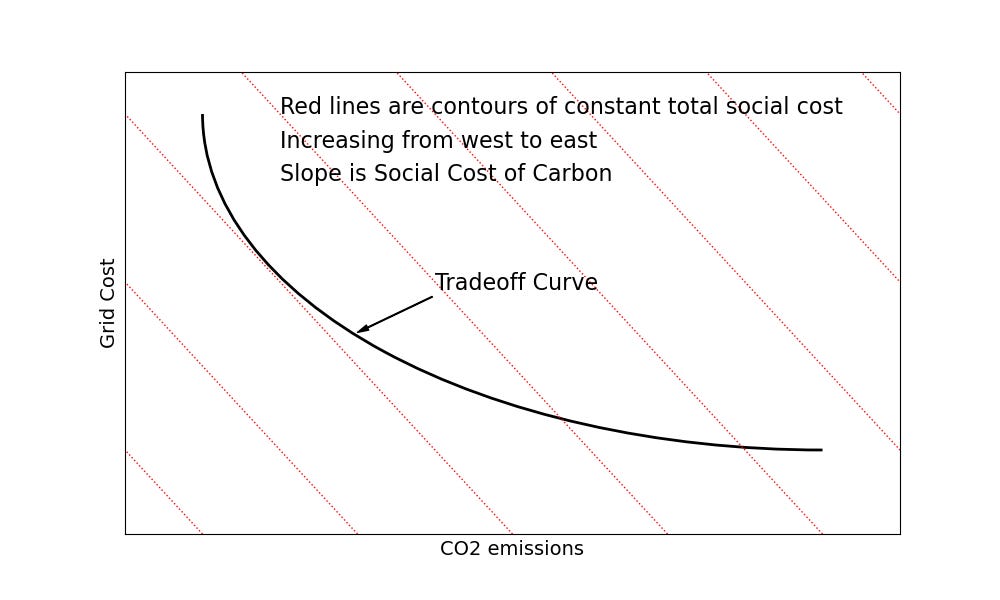

The fundamental assumption of cost-benefit analysis is that you can convert non-market disbenefits to a dollar value, in which case societal welfare is maximized by minimizing the sum of the market cost and non-market costs. This leads to the concept of a trade-off curve.

The Gordian Knot Group has used its Grid Model, to come up with a set of CO2/market cost trade off curves for Germany, varying the cost of nuclear power. Figure 1 shows the German tradeoff curve for a nuke overnight cost of $8000/kW.

The vertical axis shows the market cost of the power for that grid. On the horizontal axis, we have CO2 emissions per kWh. We want to minimize both. But we cannot. However, if we are not stupid, we can avoid solutions for which it is possible to reduce both dollar cost and CO2. But there is a frontier below which we cannot go, solutions for which you can’t further reduce CO2 with increasing dollar cost, and vice versa. That frontier is the trade off curve.

Underlying each point on that curve is the combination of wind, solar, coal, gas, nuclear, batteries, and hydrogen that produced that point. The inset shows the grid that the GKG model came up with for the 8K nuke cost and a Social Cost of CO2 of $100/ton. The blue bars show the installed capacity of each technology. The hashed portion of the blue bars shows the portion of that capacity which produced marketed power. The red bars shows the CO2 emitted by each technology. Each point on the trade-off curve will have its own optimal grid.

Once we are down on the trade off curve, society must pick pick a point on it. If you think that the cost to society of a unit of CO2 emission is extremely high, you pick a point where the slope of the trade off curve is very high, a point on the far left side of the curve. If you think the social cost of CO2 is very low, you opt for a point where the slope of the curve is very low, a point on the far right side of the curve. Whatever point you pick, the slope of the curve at that point is your effective Social Cost of Carbon. In other words, you have an effective Social Cost of Carbon whether you can articulate it or not. We can turn that around, if you are willing to articulate your Social Cost of Carbon(SCC), you should pick the point on the trade-off curve whose slope is equal to your SCC.

Of course, anybody who claims he knows what the social cost of carbon is is either a fool or trying to fool you (aka liar). But if you are a Bayesian, --- deep down we are all Bayesians whether we admit it or not --- you can determine your probability density function (PDF) for your SCC by choosing between a series of lotteries. In doing so, there is nothing to stop you from coming up with a fat-tailed density for your PDF. The next step is to find the point on the trade-off curve that is consistent with your SCC PDF. If a dollar of carbon cost is the same as a dollar of market cost, societal welfare will be maximized by minimizing the expected total social cost (sum of market cost and CO2 cost) of producing electricity:

where p(SCC) is the SCC density, C(grid) is the market cost of a specific grid, and co2(grid) is the tons of CO2 that that grid emits.1But neither the market cost of each grid nor its CO2 emissions depends on the SCC. So this is the same as

The integral on the left is 1.00 and the one on the right is simply the mean of his PDF

where M is the mean of p(SCC). Pretend I was able to label this Equation M.

In words, our Bayesian needs to minimize the weighted sum of grid cost dollars and tons of SCC. Further the weight that he should give to a ton of SCC versus a dollar of grid cost in performing this optimization is the mean of his SCC density.

A weighted sum of dollars and CO2 tons with weight M, is a straight line with a slope of M on the trade-off curve diagram. The quick sketch below reveals that the point on the trade-off curve that minimizes such a weighted sum must have a slope of M. Otherwise we can move along the trade-off curve toward that equal slope point, and get a smaller weighted sum. His effective SCC and the mean of his SCC density are the same.

Nothing in this argument requires that the probability density function be thin-tailed. The only requirement is the probability density function must have a finite mean. There are PDF’s which don’t have a mean --- the Pareto density is one --- but there are a wide array of fat-tailed densities that do have a mean. Having a mean is a far weaker requirement than being thin-tailed. This is good news. The Useless Proposition logically leads either to paralysis or panic. Weitzman knew that and tried very hard to talk his way around it. But at the end of the day, the only way out that he could come up with was geoengineering.

But Equation M says much more than we can use cost-benefit analysis, even in situations in which the worst case costs are astronomically large. It give us explicit guidance on how to use an SCC PDF in any CO2 versus dollar cost-benefit analysis.

I’ll take myself as a cheap, available example. I’ve been called a climate denier. That’s not literally true. I’m sure the planet is warming; and I’m confident that a large part of that warming is from man-made GHG’s. This can’t go on forever. But it is also true I think almost all of the claims of massive near term impact range from highly unlikely to outright bogus. In short, I think we have some time, at least a century; but we need to use that time wisely to make a gradual, low disruption transition. The fact that we are doing anything but is why the Gordian Knot Group exists.

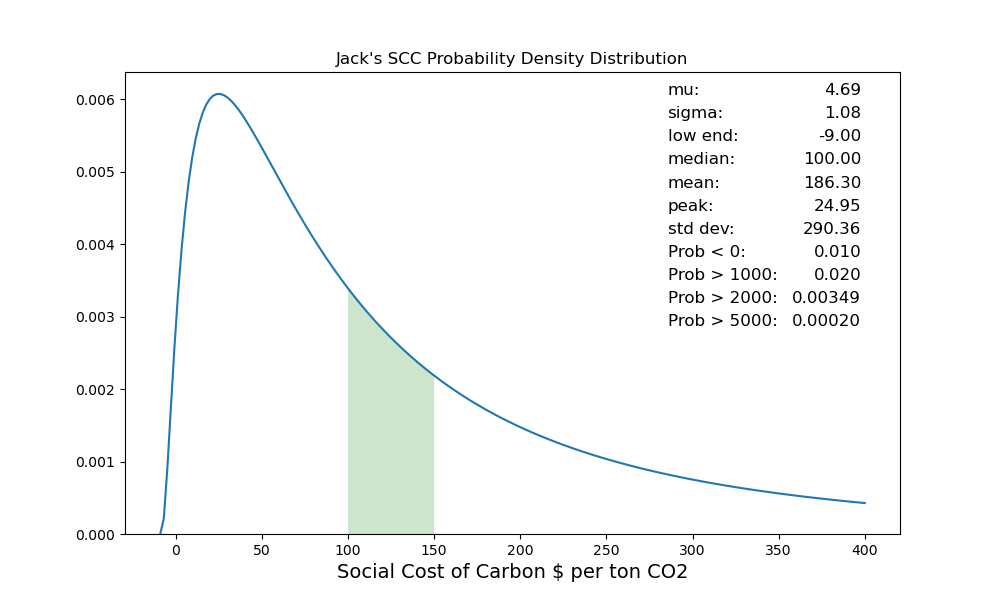

Figure 2. Jack’s Social Cost of Carbon Probability Density. The area under the density curve between any two numbers is the probability that the SCC is between those two numbers. The green area is my probability the SCC is between 100 and 150 $/ton.

Figure 2 shows my SCC PDF. It’s a log-normal with a peak near $25/ton of CO2. Most alarmists would call that number far too low. But Equation M could care less where the peak of my PDF is. It says use the mean. Fat-tailed densities can result in means that are no where near the peak. In my case, my mean is $186/ton, nearly a factor of ten larger than my peak.

That’s a big number. As a market guy, I must logically support a carbon tax equal to my SCC. Burning a gallon of gas creates about 8.9 kg of CO2. $186 a ton is 0.186 $/kg. I must support a CO2 tax on gasoline of $1.65 per gallon.2 Weitzman was right about one thing. There’s a big policy difference between thin-tailed and fat-tailed densities. But that does not mean either paralysis or panic.

Barring a philosopher king I don’t think it’s practical to work from individual SCC PDF’s to society’s SCC. Instead I would work from the trade-off curve to society’s effective SCC. Consider the electricity grid issue. In a democracy, here’s what I’d do:

1) We figure out what the trade-off curve is, and publish the curve. That’s a purely technical job, requiring no value judgements. We don’t disclose the grid behind each point on the curve.

2) We take a binding poll, asking everybody what point on the curve they like best.

3) The median of the answers is declared the societal optimum, and the slope at that point is society’s SCC.

4) We reveal the grid that produced that point. And that’s the grid we build.

5) Society has revealed its effective SCC. We use that SCC to guide all our other choices: such as a CO2 tax.

Nobody will be perfectly happy with the resulting grid, nor the chosen SCC. But it won’t be a stupid grid. It will do a good job on both cost and CO2. And the effective SCC will represent a balance of competing interests. Our decisions will be internally consistent. Compare that with what we have now.

Another assumption has crept into my argument. I’ve assumed his SCC is constant. Over a very wide range of CO2 concentrations this is not true. 20,000 years ago CO2 was at 190 ppm. That’s dangerously close to the 175 ppm level that could no longer support photosynthesis. The SCC was indisputably negative. The more CO2 the better. If CO2 concentration were double what it currently is, it’s likely he would have a higher SCC. But to the extent that the change is gradual, the argument holds.

Before you gasp, the revenues from such a large CO2 tax should replace other taxes, or can be rebated in a manner that is progressive, as suggested by Hansen.

What if CO2 emissions don’t matter.

Really solid breakdown of why Weitzman's "useless proposition" goes too far. The key insight that fat-tailed densities can still have finite means is crucial. I've wrestled with similar questions around tail risk in fintech and seeing it laid out this clearly helps a ton. The trade-off curve approch makes way more sense than the all-or-nothing framing. One thing that still bugs me is how sensitive optimal policy ends up being to that mean calculation tho.